Why Your Deals Are Falling Apart at the Finish Line (And How to Stop It)

You did everything right.

Worked the lead. Showed the homes. Got the offer accepted.

Then day 25 hits. Your lender goes quiet. Suddenly you're doing the detective work — calling, emailing, chasing. And somewhere in that chaos, the seller loses patience.

Deal dead. And you're starting over.

Here's the part nobody talks about: most deals don't die because of the market. They die because of the lender. Specifically, the wrong lender. One who was fine for 80% of deals but completely unprepared for the one in front of them.

This post breaks down the real reasons financing kills closings, and what agents who consistently protect their commissions do differently.

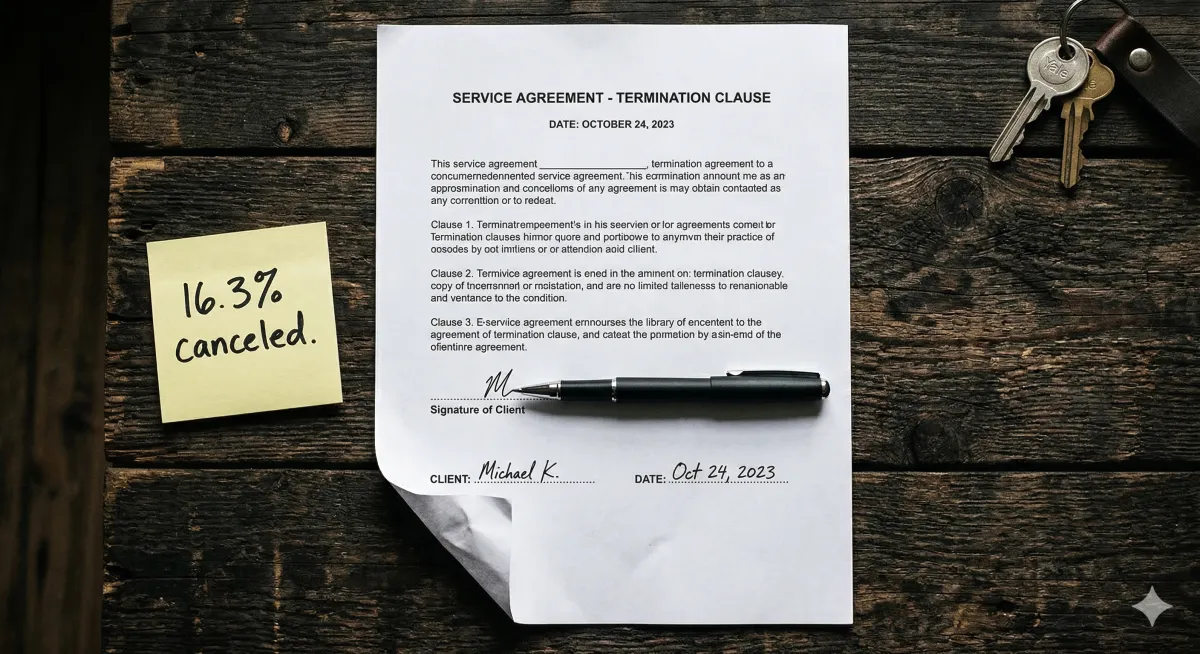

First, Let's Talk About How Common This Actually Is

According to a January 2026 Redfin analysis, 16.3% of homes that went under contract in December were canceled. That's the highest December cancellation rate since Redfin began tracking the metric in 2017.

Then in February 2026, Redfin reported January cancellations hit 13.7%— also a record for that month. The trend is clear and it's moving in the wrong direction for agents.

And that number doesn't capture the near-misses. The deals that dragged for weeks on financing delays, killing momentum, burning goodwill, and still closing. Those take a toll too.

Reason #1: The Pre-Approval Wasn't Actually Solid

This one stings because it's invisible until it isn't.

A pre-approval letter means a lender looked at the basics (income, credit, debt) and said "probably yes." It's not a commitment. It's not underwriting. And depending on who issued it, it may have been done in 20 minutes with minimal documentation.

The difference between a real pre-approval and a flimsy one shows up on day 28. Not day 3.

What actually protects your deal:

● Credit pulled and hard-verified

● Income documented (W-2s, tax returns, or profit/loss for self-employed)

● Debt-to-income calculated with the actual purchase price, not a rough estimate

● Ideally, a full credit package submitted to underwriting before the offer is even accepted

The Dwell Standard: We issue pre-approvals that are built to survive underwriting. If we flag a problem, we flag it before your client writes a check, not after they're under contract.

Reason #2: The Lender Only Had One Tool

Most lenders work with a small shelf of loan products. Conventional. FHA. Maybe VA. That's fine... until it isn't.

Your client is self-employed and write-offs make the tax returns look rough. Or they're a foreign national. Or they just switched jobs six months ago. Or their income is solid but their credit score is 612.

A lender with three options either forces that client into a product they don't fit or they call you with the news that it's dead.

Product depth isn't a nice-to-have. It's what keeps deals alive when the situation gets complicated. Which, in 2026, it often does.

See how FHA financing works for buyers with less down — that's just one of 30+ investor options Dwell can access.

What product depth looks like in practice:

● DSCR loans for your investor clients

● No Tax Return / Bank Statement loans for the self-employed

● ITIN / Foreign National programs

● Down Payment Assistance for the buyer who's close but not quite there

● Bridge loans when a client needs to move before their current home sells

● Renovation loans when the right home needs work

● Jumbo products for your high-net-worth clients who don't fit the conforming box

Reason #3: Communication Dropped Off After the Contract

This is the one that quietly destroys agent-lender relationships. Not a bad outcome, just silence.

Your client is under contract. The lender has what they need. Days pass. You ask for an update. "Working on it." More days pass. Closing is in 10 days and you still don't know where the file sits in underwriting.

According to Inman research, 59% of agents say lender responsiveness is their #1 consideration when choosing a lending partner. Not rates. Not fees. Responsiveness.

Because an agent who can't answer their client's questions looks bad. And an agent who doesn't know where their deal stands can't protect it.

Reason #4: The Appraisal Caught Everyone Off Guard

Appraisal issues kill deals in two ways:

● The home appraises below the contract price, and nobody has a plan

● The appraisal takes forever and the rate lock expires or the seller loses patience

A lender who's done this for a while knows how to get ahead of appraisal risk. They pull comps before locking the rate. They flag potential value gaps early. They have a conversation with you and your client before the appraisal is even ordered.

Surprises aren't always avoidable. But they're a lot less common when your lender is proactive instead of reactive.

Reason #5: The Client Changed Something After Pre-Approval

This one is partly on the lender. Not because they caused it, but because they didn't prevent it.

A good lender gives every client a clear 'do not do this' list the moment they get pre-approved. For the full picture of what trips buyers up, see From Application to Keys.

Buyer education at the front end is loan protection at the back end.

Reason #6: Nobody Had a Backup Plan

The deal stalled. The primary loan hit a wall. And there was no Plan B.

This is where product depth and relationship depth collide. An experienced broker with 30+ investor relationships doesn't just have one path to close. They have three or more.

If Investor A won't do it, Investor B might. The file pivots, instead of just dying.

That's the difference between a loan officer who works for one bank and a mortgage broker who works with 30+ investors. One path vs. many.

What Agents Who Rarely Lose Deals Actually Look For in a Lender

They don't just send clients to whoever offers the lowest rate that week. They have a short list of questions they've learned matter:

● "What loan products do you have access to for a client who's self-employed with complex taxes?"

● "How do you handle a deal when the appraisal comes in low?"

● "What's your average time from contract to clear-to-close?"

● "How do you communicate with me and my client during underwriting?"

● "What happens if this loan hits a wall? Do you have alternative options?"

If the lender can't answer those questions specifically... that tells you something.

Why Agents Who Work With Dwell Stop Asking Those Questions

We're not a bank. We don't work for one institution with one set of guidelines.

We're a mortgage broker with access to 30+ investors, which means 30+ sets of guidelines. When one door closes, we already have the next one open.

Our clients get:

● Real pre-approvals built to survive underwriting, not just look good on paper

● Access to every loan type on the market: conventional, FHA, VA, USDA, jumbo, DSCR, bridge, HELOC, renovation, construction, foreign national, no-doc, and more

● Proactive communication. You know where the file stands without having to ask

● No lender fees on future refinances (our Lifetime Loyalty promise to your clients)

● A team that treats your reputation like our own. Because if your deal dies, so does ours.

Ready to see it in action? Learn what a clean close looks like — then connect with me.

The Bottom Line

Deals fall apart for reasons that are mostly preventable.

We're talking: weak pre-approvals, lenders with no flexibility, poor communication after the contract, and no contingency when the loan hits a complication.

The agents who consistently close deals don't just find the right homes. They protect the transaction from the moment the offer is accepted, and that starts with who they trust to handle the financing.

Choose that partner deliberately. Your commission depends on it.